Variable vs Fixed: Which Mortgage Works in 2026?

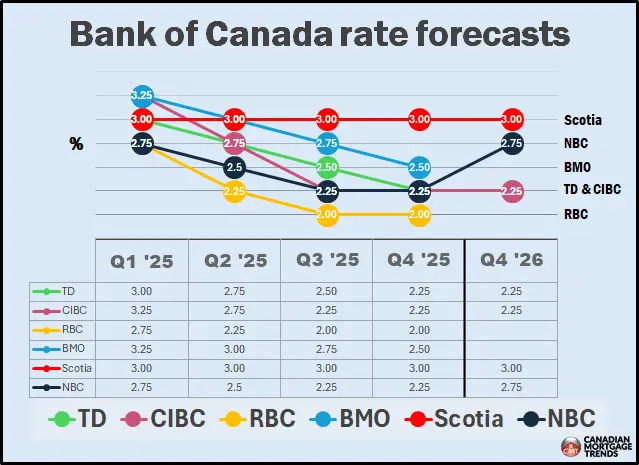

The choice between a fixed-rate and variable-rate mortgage in 2026 hinges on aligning the loan structure with your financial stability needs and expected time in the home. Fixed rates offer unchanging payments for budgeting ease, while variable rates adjust with the Bank of Canada's policy rate, potentially lowering costs if rates stabilize or fall further. Current forecasts indicate policy rates around 2.25% to 2.50%, suggesting a transition from rate cuts to stability or slight increases.

Why This Decision Matters in 2026

Canada's mortgage market in 2026 reflects a maturing rate-cut cycle, with the Bank of Canada likely pausing aggressive easing after reductions in prior years. This environment affects first-time buyers and homeowners renewing mortgages, as even minor rate shifts influence qualification thresholds and monthly cash flow. Understanding these dynamics helps borrowers avoid surprises in affordability during economic transitions.

First-time buyers, often navigating high home prices and debt loads like student loans, benefit from clarity on how mortgage types impact long-term costs. Homeowners, particularly those with tight budgets, weigh payment predictability against opportunities for savings as rates evolve.

What a Fixed Rate Actually Means

A fixed-rate mortgage sets the interest rate constant for the term, typically 1 to 5 years, ensuring principal and interest portions of payments remain steady. Payments do not fluctuate with market changes, aiding consistent household budgeting. In 2026, 5-year fixed rates are projected between 3.69% and 4.1%, influenced by bond yields rather than direct policy rate moves.

This structure suits scenarios where economic uncertainty could prompt rate hikes, shielding borrowers from immediate impacts. Lenders calculate these rates based on longer-term yield curves, providing a buffer in volatile periods.

Pros and Cons of Fixed Rates

Fixed rates deliver payment certainty, ideal for families planning expenses around fixed incomes or those sensitive to cash flow variations. They protect against rising rates, common if inflation pressures reemerge.

Drawbacks include a starting premium over variable rates and steep interest rate differential penalties for early breakage. These costs can deter frequent movers or refinancers, limiting adaptability.

What a Variable Rate Means in Today’s Market

Variable-rate mortgages tie directly to the lender's prime rate, which tracks the Bank of Canada's overnight rate plus a spread. Payments or principal allocations adjust as prime changes, with some products capping increases. Forecasts for 2026 show prime rates stabilizing near 4.75% to 5.00% if policy holds.

Lenders may recalculate monthly payments or redirect excess to principal during rate drops, accelerating equity buildup. This responsiveness suits declining or flat rate periods but exposes borrowers to upward moves.

Pros and Cons of Variable Rates

Variable rates historically yield lower total interest in stable or falling environments, starting below fixed equivalents. In 2026's projected steady rates, they offer automatic savings without refinancing.

Risks involve payment hikes during rate rises, challenging tight budgets, and psychological strain from uncertainty. They demand financial flexibility for potential increases.

2026 Market Reality: How the Environment Favors Each Option

Stable to modestly rising rates in 2026 favor fixed for long-term holders seeking insulation from hikes. Variable appeals where further easing occurs or short holds allow capturing lower costs. Bond yield stabilization keeps fixed competitive, narrowing the gap.

First-time buyers often prioritize fixed for qualification comfort under stress tests. Homeowners renewing face choices based on renewal timing amid these forecasts.

Timeline Matters: How Long You Plan to Stay in the Mortgage

-

1–3 years: Variable often edges out in stable rates, minimizing total interest.

-

3–5 years: Balance risk; fixed if hikes loom, variable for flexibility.

-

5+ years: Fixed supports steady planning amid uncertain cycles.

Comparing Costs: Practical Example

On a $500,000 mortgage over 25 years, a 0.25% rate drop saves roughly $80–$120 monthly, or $960–$1,440 yearly. In 2026, such shifts underscore variable's potential in pauses but fixed's safeguard against reversals.

How to Choose Based on Your Situation

Fixed suits those valuing predictability, with limited buffers, or long horizons. Variable fits flexible budgets, short terms, or rate-decline bets. Assess via stress tests and personal forecasts.

💬 Reach out anytime:

📞 Call or text: 236-457-4230

📧 Email: rico@mypropertycentral.ca

🌐 Website: www.riccardomanazza.realtor

🏡 Explore more lifestyle stories: livingintheokanagan.ca

🤝 Team & listings: mypropertycentral.ca

📅 Book a meeting: Book A Call with Rico

Let’s Stay Connected

If you enjoyed this article or want to stay in touch with what’s happening in the South Okanagan real estate market, let’s connect online:

📸 Instagram: @riccardo_manazza_exp-realty

📘 Facebook: @riccardo.manazza.exp

💼 LinkedIn: Riccardo (Rico) Manazza

Follow for weekly market updates, behind-the-scenes insights, and tips from one of the Most dedicated REALTORS® in the Okanagan with eXp Realty and the My Property Central Real Estate Group.

For immediate assistance or to schedule a showing, contact my assistant (available 24/7) at 236-500-6778.

Disclaimer

This article is for informational purposes only and should not be considered financial or legal advice. Eligibility criteria and program details are subject to change. Always consult with a qualified mortgage professional and licensed REALTOR® for the most current information

Categories

- All Blogs (76)

- Buyer Guidance (3)

- Buyer Guides (2)

- Buyer Resources (1)

- Buying Tips (3)

- Canadian Real estate Trends (3)

- Construction & Material Costs (2)

- Contracts & Consumer Protection (1)

- Downsizing (1)

- Economic Insights (2)

- Estate Planning & Finance (1)

- Featured Listings (2)

- Financial Education (1)

- Financial Planning for Homebuyers (2)

- First time Buyer Advice (4)

- Home buying advice (7)

- Home Buying Guides (3)

- Home Selling Strategies & Market Insights (1)

- Home Selling Tips & Market Insights (1)

- Homeowner Advice (3)

- Homeownership Tips (1)

- Housing Market Analysis (1)

- Interest Rates & Financing (1)

- Investment & Lifestyle Real Estate (1)

- Investment Strategies (2)

- Legal & Probate Guidance (1)

- Listings in Oliver (1)

- Market Trends (1)

- Market Education (1)

- Market Updates (15)

- Mortage & Financing (2)

- Mortage Strategies (2)

- Okanagan Lifestyle & Local Guides (2)

- Osoyoos Real Estate (3)

- Penticton & Okanagan Housing Market Analysis (1)

- Penticton Real Estate (4)

- Pet-Friendly Homes (1)

- Probate & Estate Real Estate (1)

- Probate Real Estate (1)

- Real Estate Business & Motivation (1)

- Real Estate Career & Client Education (1)

- Real Estate Career & Motivation (2)

- Real Estate Career Insights (1)

- Real Estate Education (1)

- Real Estate Financing & Investment (1)

- Real Estate Guides (3)

- Real Estate Insights & Guides (3)

- Real Estate Investment & Market Insights (1)

- Real Estate Investment Analysis (1)

- Real Estate Investment Strategies (1)

- Real estate Market insights (1)

- Real Estate Market Updates (1)

- Real Estate Tips (5)

- Real Estate Trends (1)

- Remember to Create (1)

- Seller Guides (1)

- Seller Resources (1)

- Seller Tips (1)

- Selling Tips (2)

- South Okanagan Insights (1)

- South Okanagan Listings (1)

- South Okanagan Market Reports (2)

- South Okanagan Market Update (4)

- South Okanagan Real estate (11)

- South Okanagan Real Estate Investing (3)

- South Okanagan Real Estate Market (2)

- Sustainable Real Estate Investing (1)

- Townhouse Oliver (1)

Recent Posts